[ad_1]

TL;DR:

The UK authorities has revealed a set of proposals for the regulation of the crypto sector for public session. The proposals cowl the authorization of crypto companies and the sorts of necessities to be imposed on them. Importantly, it units out the actions that, along with stablecoins, might be regulated within the UK. These are: Cryptoasset Issuance and Disclosure Regime, Working a Cryptoasset Buying and selling Venue, Cryptoasset Intermediation Actions, Cryptoasset Custody, Working a Cryptoasset Lending Platform, and Common Market Abuse Necessities.

WATCH: A Video summarising the UK’s Crypto Proposals

Introduction

If 2022 was the 12 months of high-profile crypto failures, then 2023 is shaping as much as be the 12 months of crypto regulation. A mix of the maturation of the crypto sector as an necessary one attracting nice curiosity from institutional and retail buyers alike and rising unease with the dearth of regulatory oversight signifies that it’s now not tenable for public policymakers to disregard the sector.

On 1 February 2023, the UK authorities, by way of its Ministry of Finance (HM Treasury), revealed the eagerly awaited session paper setting out its proposed strategy to the regulation of cryptoassets within the UK. The doc, titled: “Future monetary companies regulatory regime for cryptoassets,” is designed to assist make the UK a secure vacation spot for crypto exercise and innovation. The session closes for feedback on 30 April 2023.

On this article, we offer a complete overview of the proposals, which cowl:

The UK’s Coverage Goals and Design Ideas

Definition of Cryptoassets

Cryptoasset Actions

Cryptoasset Issuance and Disclosure Regime

Working a Cryptoasset Buying and selling Venue

Cryptoasset Intermediation Actions

Cryptoasset Custody

Working a Cryptoasset Lending Platform

Common Market Abuse Necessities

The UK’s Coverage Goals and Design Ideas

In keeping with the prevailing regimes for conventional monetary companies, the UK intends to control the monetary companies actions of the crypto sector reasonably than the property themselves. This goals to scale back the danger of “regulatory arbitrage,” i.e., companies structuring merchandise or devices specifically methods to avoid monetary companies rules.

Till now, the absence of a regulatory framework for crypto within the UK has meant that crypto startups have been in a position to create platforms for offering monetary companies with out first acquiring regulatory licences for these. Merely put, there was no chance of acquiring such licensing as a result of absence of a legislative/regulatory framework and restraint from UK regulatory our bodies.

It’s price stating on the outset that, as soon as handed into legislation, the proposals will imply that authorized individuals (i.e., people and entities) wishing to hold out sure actions within the crypto sector would require prior authorization underneath Half 4A of the Monetary Providers and Markets Act 2000 (FSMA) – the identical laws that governs conventional finance within the UK.

Coverage Goals

The session paper units out the 4 coverage aims underpinning the UK’s proposed strategy to the regulation of cryptoassets, that are to:

Encourage development, innovation, and competitors within the UK

Allow customers to make well-informed selections, with a transparent understanding of the dangers concerned

Defend UK monetary stability.

Defend UK market integrity

Design Ideas

Equally, three core design ideas information the UK’s strategy, that are:

Identical danger, similar regulatory end result

Proportionate and centered

Agile and versatile

In its bid to guard UK customers and guarantee monetary stability, it’s clear that the UK authorities desires a sure equality of outcomes relative to comparable actions carried out by conventional finance (TradFi) companies however acknowledges that crypto could require a unique regulatory strategy. The UK additionally desires a versatile strategy that allows regulators to adapt and evolve to adjustments within the crypto market in addition to developments in worldwide regulatory requirements.

These fearing a draconian regulatory strategy could also be inspired by the truth that the UK plans to deal with addressing pressing or acute dangers and alternatives. That’s, it would purpose to keep away from imposing disproportionate rules, particularly when end-users are conscious of the dangers concerned and the actions don’t pose a menace to market integrity or monetary stability.

Definition of Cryptoassets

Traditionally, the UK has tended to keep away from the phrase “forex” when referring to cryptocurrencies, therefore the identify “cryptoasset.” It believes solely fiat currencies issued by governments qualify for such a designation. For consistency, on this article, we keep away from the time period “cryptocurrency,” however we do use the phrases “crypto” and “cryptoasset” interchangeably.

The UK has already outlined cryptoassets within the draft Monetary Providers and Markets Invoice 2022 (FS&M Invoice), which is presently going by means of parliament (and addresses fiat-backed stablecoins, amongst different issues).

A cryptoasset is outlined as:

“any cryptographically secured digital illustration of worth or contractual rights that—

(a) might be transferred, saved or traded electronically, and

(b) that makes use of expertise supporting the recording or storage of knowledge (which can embrace distributed ledger expertise).”

This definition is deliberately broad in order to seize all present sorts of cryptoassets and be versatile sufficient to cowl any digital property that could be created however which aren’t primarily based on a distributed ledger or blockchain expertise. Nonetheless, there may be recognition that the definition could should be up to date sooner or later to maintain up with developments within the sector. Subsequently, the FS&M Invoice contains the ability for the federal government to replace the definition by way of secondary laws if wanted.

However the broad definition, because the UK is adopting an activities-based strategy (reasonably than looking for to control the property themselves), the session paper clarifies that precise regulatory necessities will sometimes apply to a specific subset of cryptoassets relying on the matter being regulated, i.e., a narrower definition might be used to seize these.

Cryptoasset Actions

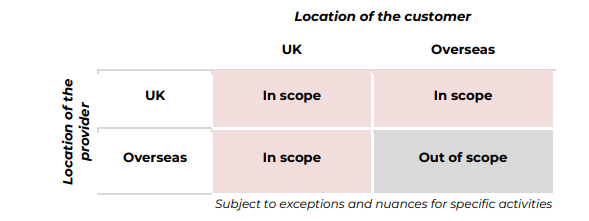

Understandably, the UK authorities plans to seize regulated actions supplied by UK companies to prospects “in” the UK (or overseas) in addition to these supplied by international companies “to” prospects in the UK.

Geographic scope of cryptoasset actions captured by the UK’s proposals

Given the borderless nature of the web and the truth that UK prospects could select to entry companies supplied by international companies, there’ll possible be an exemption for so-called “reverse solicitation” to cowl situations wherein a UK buyer decides to entry a cryptoasset service “completely at their very own initiative from an abroad agency and the agency doesn’t in any other case solicit from such prospects.” This is able to not require UK licensing underneath the FSMA for that abroad agency.

Though topic to alter following the session course of, the next are the proposed scope of cryptoasset actions to be regulated within the UK.

The UK’s proposed scope of cryptoasset actions to be regulated

Class of Exercise

Indicative sub-activities

Issuance actions

Issuance and redemption of a fiat-backed stablecoin

Admitting a cryptoasset to a cryptoasset buying and selling venue

Making a public provide of a cryptoasset

Fee actions

Execution of fee transactions or remittances involving fiat-backed stablecoins

Change actions

Working a cryptoasset buying and selling venue which helps:

the change of cryptoassets for different cryptoassets

the change of cryptoassets for fiat forex

the change of cryptoassets for different property (e.g. commodities)

Funding and danger administration actions

Dealing in cryptoassets as principal or agent

Arranging (bringing about) offers in cryptoassets

Making preparations with a view to transactions in cryptoassets

Lending, borrowing and leverage actions

Working a cryptoasset lending platform

Safeguarding and /or administration (custody) actions

Safeguarding and/or administering (or arranging) a fiat-backed stablecoin, technique of entry to the fiat-backed stablecoin (custody), or different cryptoassets

The desk above is indicative at this stage and might be amended in the end. Different actions may be added. Notice that the session paper additionally contains Requires Proof on plenty of areas e.g. Decentralized Finance (DeFi) (however that is exterior the scope of this text). The proof gathered will then be utilized by the UK authorities to affect the way it proceeds in these areas.

Different areas that will in future fall throughout the UK’s scope of cryptoasset actions to be regulated

Class of Exercise

Indicative sub-activities

Change actions

Submit-trade actions in cryptoassets (to the extent not already coated)

Funding and danger administration actions

Advising (to the extent not already coated) on cryptoassets

Managing (to the extent not already coated) cryptoassets

Validation and governance actions

Mining or validating transactions, or working a node on a blockchain

Utilizing cryptoassets to run a validator node infrastructure on a proof-of-stake (PoS) community (layer 1 staking)

Cryptoasset Issuance and Disclosure Regime

The UK authorities proposes to ascertain an issuance and disclosure regime for cryptoassets that’s modelled on the ‘UK Prospectus Regime’ (which is itself set to be reformed shortly) however tailor-made to the particular attributes of cryptoassets. The design of the regime borrows from current TradFi regimes for ‘Multilateral Buying and selling Facility (MTF)’ and public provide platform disclosures. The next actions will function the triggers for the operation of the longer term UK crypto regime:

Admitting (or looking for admission of) a cryptoasset to a cryptoasset buying and selling venue; or

Making a public provide of a cryptoasset (together with ICOs), which might should be carried out by way of a regulated platform.

Which means that itemizing a coin on a crypto change or conducting an Preliminary Coin Providing (ICO) will, sooner or later, be topic to the availability of a minimal normal of knowledge, in addition to different investor safety measures round advertising and marketing supplies and commercials.

An software for admission onto a buying and selling venue (i.e., a crypto change) will should be assessed in accordance with the venue’s detailed admission necessities, which is able to, in flip, be topic to overarching ideas which the regulatory physique, the Monetary Conduct Authority (FCA), will set out. The issuer might want to make public disclosures akin to a prospectus – one thing the crypto sector is comparatively conversant in (i.e., whitepapers). Nonetheless, not like whitepapers which can differ wildly in kind and substance, a crypto issuance/itemizing disclosure doc must present a minimal set of knowledge necessities, round:

the options, prospects, and dangers of the cryptoassets

the rights and obligations connected to the cryptoassets (if any)

a top level view of the underlying expertise (together with protocol and consensus mechanism)

if relevant, the particular person looking for admission to buying and selling on a cryptoasset buying and selling venue

Apart from the disclosure necessities to be imposed on the time of itemizing, there could also be a necessity for ongoing disclosure necessities to be imposed on companies (such ‘persevering with obligations’ are normal in TradFi for listed public corporations). As an example, crypto companies could must disclose key occasions comparable to Code Audits, adjustments to the way in which a cryptoasset capabilities (e.g., the current Ethereum Merge), and so forth.

Understandably, these disclosure paperwork will include authorized and regulatory legal responsibility connected for negligence or omissions. Controversially, nevertheless, the place the cryptoasset in query doesn’t have an issuer (as a result of it’s generated by a public, permissionless blockchain platform comparable to Bitcoin), the change wishing to checklist it will want to arrange the disclosure paperwork itself and, importantly, assume legal responsibility. Assuming legal responsibility for unfaithful or deceptive statements or for omissions could lead to a disproportionate burden for exchanges since they don’t have any management over such platforms.

Working a Cryptoasset Buying and selling Venue

The UK authorities proposes to ascertain a regulatory framework that’s primarily based on current actions round regulated buying and selling venues (e.g., the operation of an MTF). For TradFi, that is presently set out within the Regulated Actions Order (RAO), a key piece of secondary laws within the UK monetary companies sector.

As soon as the exercise of Working a Cryptoasset Buying and selling Venue turns into a regulated exercise underneath the RAO, it signifies that any crypto change wishing to function within the UK (or provide its companies to UK prospects) would require authorization by the FCA. Licensed companies might be required to satisfy varied necessities, together with the next:

Prudential necessities – minimal capital and liquidity necessities to satisfy each ‘going concern’ and ‘gone concern’ wants.

Shopper safety – managing conflicts of curiosity, dealing with buyer complaints, and guaranteeing truthful and clear entry guidelines and price schedules.

Governance necessities – exchanges might want to have strong governance preparations in place (unsurprising that it will have even better significance going ahead, given the continued FTX debacle).

Operational resilience necessities – methods & controls, folks and processes, outsourcing preparations, enterprise continuity, catastrophe restoration preparations, and cyber safety.

Information reporting – functionality to readily present correct and full data for each on- and off-chain transactions.

Decision and Insolvency – FCA participation in insolvency proceedings and doubtlessly a bespoke decision regime might be developed sooner or later (just like that relevant to TradFi companies).

Cryptoasset Intermediation Actions

Naturally, for intermediation actions (e.g., market making), the proposals draw inspiration from current RAO-based regulated actions in TradFi. For instance, the TradFi exercise of “arranging offers in investments” simply interprets into “arranging (bringing about) offers in cryptoassets,” and so forth.

Nonetheless, there could also be a necessity for added necessities to deal with specificities of the crypto market, e.g., conflicts of curiosity could come up from extra vertically built-in cryptoasset enterprise fashions. It is because crypto exchanges are likely to conduct actions aside from purely working a buying and selling venue (comparable to custody, post-trade actions, proprietary buying and selling, lending, issuance of personal native cryptoasset, and so on.).

Just like the sorts of necessities that might be imposed on exchanges above, these companies wishing to have interaction in intermediation actions might want to meet necessities round authorization/licensing, prudential soundness (capital and liquidity, and so on.), client safety & governance necessities (conflicts of curiosity, transparency, suitability), operational resilience, information reporting, in addition to decision and insolvency issues.

It’s price noting that the idea of “greatest execution” – which is sort of acquainted to these concerned in TradFi – can even prolong to crypto, i.e., crypto companies might be required to take all affordable steps to acquire the “very best consequence for the shopper when executing a shopper order.”

Cryptoasset Custody

In contrast to crypto exchanges and stablecoins issuers, earlier public statements across the potential for crypto sector regulation have tended to focus much less on custody. Subsequently, it’s particularly welcome that the UK’s proposals for crypto regulation handle custody straight. It is because, because the session factors out:

“Custody represents one of many key elements of the cryptoasset lifecycle by way of offering buyers entry to, and secure storage of, their property.”

To additional buttress the necessity for strong regulatory necessities round custody, the session states:

“with out clear and tailor-made regulatory requirements to which companies are required to stick, cryptoassets might not be safeguarded adequately, resulting in danger of losses ought to the agency enter insolvency (both as a consequence of the property being handled as property of the agency or as a result of loss, fraud or operational errors). Along with the hurt to buyers, an end result that leads to uncertainty in insolvency might additionally influence confidence out there.”

The session signifies that crypto custodians will possible be required to make sure ample preparations to safeguard buyers’ rights to their cryptoassets. Custodians can even want to ascertain clear processes for redress within the occasion that cryptoassets held in custody are misplaced.

Nonetheless, maybe disappointingly for retail prospects specifically, the UK will possible fall wanting requiring full legal responsibility within the occasion of lack of shopper property. Whereas the suitable legal responsibility requirements for custodians are nonetheless into consideration, the UK authorities is exploring taking an strategy that won’t impose full, uncapped legal responsibility on the custodian within the occasion of a malfunction or hack that was not throughout the custodian’s management.

However the possible absence of full legal responsibility, having clear guidelines in place which set out the circumstances underneath which custodian legal responsibility would exist and to what extent might be extraordinarily helpful. And in any occasion, this may increasingly open up aggressive pressures on companies providing custody companies to transcend the regulatory minimal requirements by establishing further redress strategies, e.g., by way of third-party insurance coverage.

Corporations offering custody companies might want to meet necessities round authorization/licensing, prudential soundness (capital and liquidity, and so on.), client safety & governance necessities (shopper disclosures, clear contractual phrases, and whether or not Monetary Providers Compensation Scheme (FSCS) safety is offered for claims – one thing the FCA will decide, operational resilience, information reporting, in addition to decision and insolvency issues.

As well as, such companies can even want to satisfy custody-specific necessities across the safeguarding of shopper property just like these required of TradFi custody banks (set out within the FCA’s Consumer Property Sourcebook (CASS)). These necessities purpose to guard purchasers in each ‘going concern’ (i.e., buyers’ rights to their property) and ‘gone concern’ (to make sure that property are returned to buyers promptly and as entire as potential).

Working a Cryptoasset Lending Platform

The current failures of centralized crypto companies, Celsius, BlockFi, and FTX, have in all probability created the impetus for addressing crypto lending presently. Corporations engaged in lending actions are uncovered to credit score and liquidity dangers, and but cryptoasset lending and borrowing actions performed by lending platforms sometimes fall exterior the present regulatory perimeter.

Subsequently, the UK authorities plans to introduce a crypto lending regime that can embrace necessities round efficient danger administration of collateral and contingency planning for the failure of individuals’ largest market counterparties. To facilitate this, a newly outlined regulated exercise might be created for “working a cryptoasset lending platform.”

Nonetheless, in a curious break from the federal government’s acknowledged design precept of “similar danger, similar regulatory end result,” the proposed strategy to crypto lending is not designed to attain the identical outcomes as these out there in current TradFi lending actions, e.g., FSCS safety, affordability assessments and forbearance durations.

For the longer term regulated exercise of Working a Cryptoasset Lending Platform, the UK authorities needs to attain the next outcomes:

“lending platforms ought to have ample danger warnings for customers lending to stated platform (e.g., that the buyer might lose all their cash, readability on lack of FSCS safety)

lending platforms ought to have ample monetary assets – capital and liquidity – and wind down preparations to hold out their enterprise

lending platforms ought to have clear contractual phrases on possession and, if relevant, ringfencing of retail funds in case of insolvency”

The intention is to attain these by means of a mixture of necessities round authorization/licensing, prudential soundness (capital and liquidity, and so on.), client safety (shopper disclosures, danger warnings, clear contractual phrases together with possession of authorized and helpful title, collateral necessities and margin calls) governance preparations and danger administration processes, operational resilience, information reporting, in addition to decision and insolvency issues.

Common Market Abuse Necessities

Like TradFi, the crypto sector has attracted its justifiable share of inappropriate actors and behaviours. Suspicions and accusations abound of abuse of insider data and different market manipulation actions, e.g., so-called ‘rug-pulling.’

Additional, given the dearth of regulatory oversight, and the complexity of some crypto platforms, it may be argued that the alternatives for market abuse by venture insiders and influential characters presently exceed tolerable or ‘acceptable’ ranges.

The UK authorities admits that the globalized, fragmented, and borderless nature of crypto markets makes the policing of market abuse more difficult than for TradFi markets. In contrast to, say, fairness and glued revenue markets, the place there are particular, concentrated markets the place nearly all of buying and selling happens, there are tons of of crypto exchanges all over the world on which 1000’s of crypto tokens are traded.

The session proposes a Cryptoassets Market Abuse Regime, which imposes obligations on sure market participation, e.g., exchanges (cryptoasset buying and selling venues) that might be anticipated to “detect, deter, and disrupt market abusive behaviours.” That’s, an change could be anticipated to establish offenders, share data with different exchanges that checklist the identical cryptoassets, and publicly blacklist offenders.

The UK hopes that, by putting such important market abuse obligations on exchanges reasonably than on the FCA, exchanges could be incentivized to develop revolutionary technological approaches for detecting market abuse behaviours within the crypto sector.

Beneath is a abstract of the proposed design options for a Cryptoasset Market Abuse Regime.

Scope of offences – just like TradFi markets, civil legislation offences of market abuse would come with insider dealing, market manipulation, and illegal disclosure of inside data.

Enforcement mechanism – exchanges to be required to have processes for disrupting occurrences of market abuse exercise in their very own market.

Obligations on buying and selling venues – these could embrace Know Your Buyer (KYC) necessities, public blacklists, order guide surveillance, submission of suspicious transaction and order experiences (STORs), use of blockchain analytics, ongoing public disclosures, and so on.

Obligations for different market individuals – all regulated crypto companies might be required to reveal inside data and preserve insider lists (that is stricter than TradFi, the place solely issuers are required to take action).

Requesting the admission of a cryptoasset to a UK cryptoasset buying and selling venue would be the regulatory set off level for the appliance of the Cryptoasset Market Abuse Regime. The regime would apply no matter whether or not the market abuse exercise takes place throughout the UK or abroad.

In Conclusion,

The proposals for crypto regulation symbolize a elementary shift within the UK’s public coverage strategy to the nascent crypto sector. Along with stablecoin issuers (for which the legislative course of is already underway), the deal with exchanges, custodians, intermediation, and lending actions is smart.

As a jurisdiction looking for to ascertain itself as a significant crypto centre, the UK’s proposals needs to be welcomed as a vital step in establishing a complete regulatory framework for the monetary companies elements of crypto.

The proposed strategy of regulating actions (reasonably than looking for to control the property themselves) is vastly constructive and maintains uniformity with the regulation of conventional finance actions. It additionally avoids a dangerous try to control cryptoassets generated by decentralized, public, and permissionless platforms.

That stated, the proposal to require exchanges wishing to checklist issuer-less property (e.g., Bitcoin) to not solely put together disclosure paperwork but in addition assume legal responsibility for the accuracy of the data is arguably extreme.

Lastly, the proposals are a vastly constructive motion that seeks to stability the will to put crypto throughout the current UK monetary companies regulatory framework (legalism), the precept of reaching equal regulatory outcomes vis-à-vis conventional finance regimes (ideology), and the necessity to take account of novel options of crypto’s expertise and sectoral idiosyncrasies (pragmatism).

If you need to learn extra articles like this, go to DeFi Planet and observe us on Twitter, LinkedIn, Fb, Instagram and CoinMarketCap Neighborhood.

“Take management of your crypto portfolio with MARKETS PRO, DeFi Planet’s suite of analytics instruments.”

[ad_2]

Source link