[ad_1]

Selecting between several types of investments can really feel like navigating an unlimited sea and not using a compass, particularly for these new to the world of finance. Certificates of deposit (CDs) and bonds are each common funding choices, usually characterised as low-risk investments. However which one could be higher suited on your monetary targets? Let’s delve into this journey, evaluating CDs and bonds, demystifying their advantages, and explaining how every works intimately.

Diversification is certainly the cornerstone of any strong funding portfolio. Eager on including some crypto to your monetary combine? Changelly is your go-to resolution. Providing minimal charges and speedy transactions, it’s the last word gateway to the world of cryptocurrencies. Embark in your crypto funding journey at the moment with Changelly!

Understanding Certificates of Deposit (CDs): What are CDs?

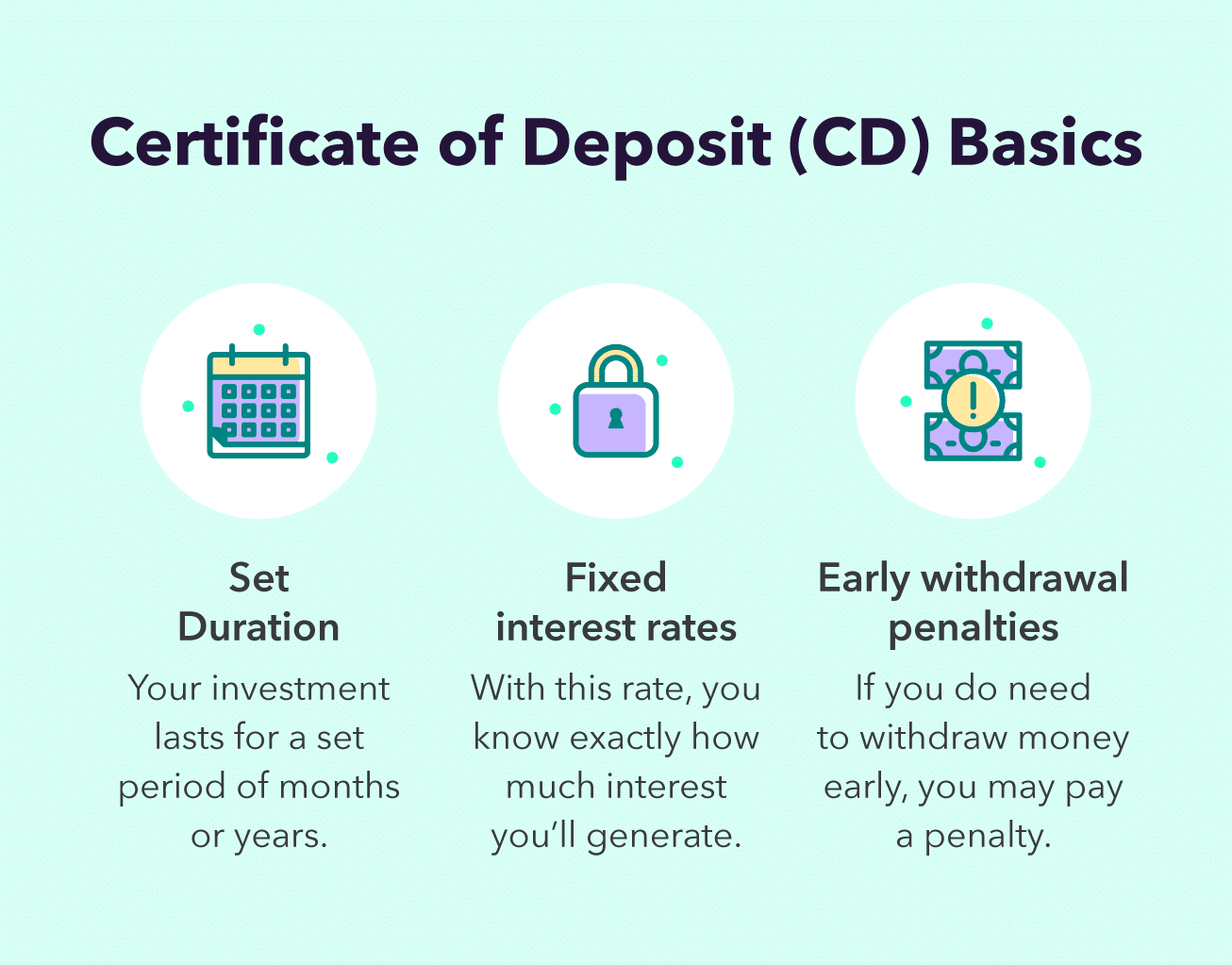

A Certificates of Deposit, or CD, is a kind of financial savings account provided by banks and credit score unions. In contrast to a daily financial savings account, a CD holds a hard and fast amount of cash for a hard and fast interval. The interval, sometimes called the “time period,” can range from a number of months to a number of years. In return for agreeing to depart your cash untouched for this time period, the monetary establishment pays you curiosity. Nonetheless, there’s a catch — if you might want to withdraw your funds earlier than the time period ends, you’ll face an early withdrawal penalty.

Varieties of CDs

The world of CDs is kind of numerous, with a number of sorts obtainable:

Conventional CDs: That is the usual kind of CD that most individuals are conversant in. You deposit your cash for a hard and fast time period and earn curiosity at a hard and fast charge. When the time period ends, you get again your preliminary deposit plus the gathered curiosity. In the event you withdraw your funds early, you’ll usually incur an early withdrawal penalty.

Bump-Up CDs: These give you the prospect to lift your rate of interest in the course of the time period if the charges within the wider market enhance. It’s a technique to hedge in opposition to potential rises in rates of interest. Nonetheless, the preliminary charge is normally decrease than the speed provided on conventional CDs.

Liquid CDs: These are extra versatile than conventional CDs as a result of they can help you withdraw a part of your deposit with out paying an early withdrawal penalty. That mentioned, their rates of interest are usually decrease, and there could also be particular guidelines about when and the way a lot you possibly can withdraw.

Zero-Coupon CDs: These kind of CDs don’t pay out curiosity yearly or semi-annually like conventional CDs. As an alternative, they routinely reinvest the curiosity earned, which implies you obtain a lump sum cost (authentic deposit plus curiosity) on the finish of the time period.

Callable CDs: These CDs could be ‘known as’ or redeemed by the issuing financial institution earlier than the time period ends, usually when rates of interest fall. This implies you could not get the complete curiosity if the financial institution decides to name the CD.

Brokered CDs: Brokered CDs are purchased through a brokerage agency, slightly than straight from a financial institution. Regardless of being initiated by banks, their promoting is outsourced to corporations, sparking competitors and usually larger yields than conventional CDs. Brokered CDs provide extra flexibility, although this could enhance the potential for funding errors.

Within the debate of CDs vs bonds, it’s value noting that CDs, aside from providing a hard and fast rate of interest assured by the financial institution, are insured by the FDIC, whereas bonds can provide doubtlessly larger yields however carry various levels of danger based mostly on the issuer.

How Secure Are CDs?

CDs are extensively considered one of many most secure funding choices obtainable. Issued by banks or credit score unions, they’re insured as much as $250,000 per depositor by the Federal Deposit Insurance coverage Company (FDIC) or the Nationwide Credit score Union Administration (NCUA). Because of this even within the occasion of the monetary establishment failing, you gained’t lose your deposit.

When Is a CD Your Finest Choice?

In my skilled view, there are specific eventualities the place a CD could be a wonderful alternative:

Outlined Brief-Time period Targets: When you’ve got a concrete aim on the horizon — a down cost for a house, a brand new automobile, or perhaps a dream trip — and also you’ve diligently saved for this goal, a CD might function a useful vessel for this nest egg. Due to its mounted rate of interest, a CD ensures that your cash will develop with none danger of market fluctuations. Nonetheless, be sure that your saving timeline aligns with the CD’s time period to keep away from an early withdrawal penalty.Need for Predictable Returns and Excessive Safety: Whenever you prioritize security and predictability, a CD shines. Your returns are spelled out from the start, and there aren’t any market situations that may jeopardize your preliminary deposit. Furthermore, the backing of the FDIC or NCUA offers you an ironclad assure that your investments, as much as $250,000, are safe even when a financial institution or a credit score union fails.

The place Can I Open a CD?

CDs could be opened at any financial institution or credit score union, and you can even purchase them by means of a brokerage agency.

Delving Into Bonds: What are Bonds?

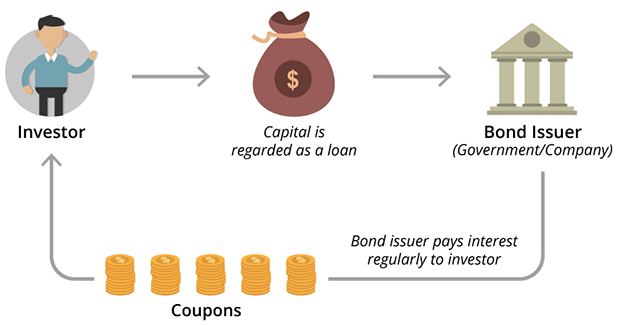

A bond is a type of mortgage that buyers make to bond issuers, which could be companies, municipalities, or the federal authorities. In return for the mortgage, the issuer guarantees to pay again the mortgage quantity, known as the “principal,” by a selected date often known as the maturity date. In the meantime, the issuer additionally makes periodic curiosity funds to the bondholder.

In the event you’re evaluating a CD vs a treasury bond, take into account that treasury bonds could also be a greater choice in case you’re on the lookout for a longer-term, lower-risk funding backed by the U.S. authorities.

Varieties of Bonds

There are a number of varieties of bonds to select from:

Authorities Bonds: These are issued by the federal authorities and are sometimes thought-about the most secure kind of bond. They arrive in three varieties: Treasury Payments (T-Payments), Treasury Notes (T-Notes), and Treasury Bonds (T-Bonds). T-Payments have the shortest maturity (as much as 1 12 months), whereas T-Notes and T-Bonds have longer maturities. The curiosity earned on these bonds is exempt from state and native taxes.

Municipal Bonds: Issued by states, cities, or different native authorities entities, municipal bonds fund public tasks like faculties, highways, and bridges. The curiosity paid on these bonds is usually exempt from federal revenue tax and infrequently from state and native taxes as properly in case you dwell within the state the place the bond is issued.

Company Bonds: Corporations difficulty company bonds to lift capital for quite a lot of causes, from operational enlargement to funding analysis. These bonds normally provide larger rates of interest than authorities and municipal bonds as a consequence of their elevated danger degree. The security of the bond is dependent upon the monetary well being of the corporate.

Financial savings Bonds: These are non-marketable securities issued by the U.S. Division of the Treasury and meant for common public funding. They’re bought in small denominations and have long-term maturities. The most typical sorts are Collection EE and Collection I financial savings bonds.

Company Bonds: These bonds are issued by government-sponsored enterprises (GSEs) and federal companies. They’re thought-about barely riskier than Treasury bonds however safer than company bonds.

Overseas Bonds: These are bonds issued by a international authorities or a company situated exterior of your own home nation. Investing in international bonds introduces additional dangers, corresponding to forex danger, however they will provide larger returns and extra diversification.

Bond Mutual Funds: These are funds that put money into varied varieties of bonds. Bond mutual funds provide diversification {and professional} administration, however the returns and principal worth can fluctuate.

How Secure Are Bonds?

Whereas bonds are usually thought-about secure investments, their security can range. For example, company bonds carry a danger of default, which means the corporate may not be capable to make curiosity funds or return the principal. Then again, municipal bonds and financial savings bonds are backed by authorities entities and are usually thought-about very low danger.

When Is a Bond Your Finest Choice?

Drawing on my expertise, I’d suggest contemplating bonds beneath these situations:

Balancing a Inventory-Heavy Portfolio: Bonds may very well be the fitting choice in case you search to stability the chance, having already invested within the inventory market. They’ll act as a counterweight to the inherent volatility of shares, smoothing out potential tough patches and offering extra stability to your portfolio.Lengthy-Time period Common Revenue: In the event you’re drawn to the concept of your funding producing constant revenue over an prolonged interval, bonds match the invoice completely. They make common curiosity funds over their life cycle and return the preliminary funding at maturity, nevertheless it’s essential to evaluate the monetary well being of the bond issuer, particularly with company bonds, to mitigate any default dangers.

Each bonds and CDs can play pivotal roles in a diversified funding portfolio, however their suitability is dependent upon particular person monetary targets, danger tolerance, and funding timelines. It’s important to do not forget that the fantastic thing about investing lies in stability and diversification, and there may be not often a one-size-fits-all reply.

The place Can I Purchase Bonds?

You should purchase bonds by means of brokerages, bond mutual funds, or, within the case of financial savings bonds, immediately from the U.S. Treasury Division.

Please allow JavaScript in your browser to finish this kind.

Bonds vs. CDs: How Do They Work?

Let’s break down the internal workings of each CDs and bonds. Whereas they’re each generally categorized as safer funding choices, the best way they operate and serve buyers could be fairly completely different.

How CDs Work

A Certificates of Deposit (CD) operates very similar to a time-specific financial savings account. Whenever you open a CD, you deposit a hard and fast amount of cash with a monetary establishment, like a financial institution or a credit score union, for a hard and fast interval. This era, sometimes called the time period, can vary from a number of months to a number of years.

The financial institution pays you curiosity on the cash you’ve deposited. The rate of interest is usually mounted, which means it gained’t change at some stage in the time period. So, you’ll know precisely how a lot your CD will earn over its lifespan.

On the finish of the time period, the CD matures. You’ll obtain the cash you initially deposited plus the curiosity you’ve earned. In the event you withdraw your cash earlier than the tip of the time period, you’ll doubtless must pay an early withdrawal penalty, which may eat into your earnings.

CDs are insured as much as $250,000 per depositor by the Federal Deposit Insurance coverage Company (FDIC) or the Nationwide Credit score Union Administration (NCUA) in the event that they’re provided by credit score unions. This implies even when the financial institution or credit score union fails, your funding is secured.

How Bonds Work

Bonds function extra like loans — however you’re the lender. Whenever you buy a bond, you’re lending cash to the issuer of the bond. This issuer may very well be a company, municipality, or the federal authorities. In return for the mortgage, the issuer guarantees to pay you a specified charge of curiosity in the course of the lifetime of the bond and to repay the face worth of the bond (the principal) when it matures, or comes due.

The curiosity cost (additionally known as the coupon cost) is normally paid semiannually. The speed is both mounted, which means it gained’t change for the lifetime of the bond, or variable, adjusting with market situations.

Bonds’ security varies relying on the issuer. U.S. Treasury bonds, backed by the complete religion and credit score of the U.S. authorities, are thought-about the most secure. Company bonds have completely different levels of danger hinging on the monetary well being of the corporate. Municipal bonds’ security is dependent upon the monetary well being of the issuing native authorities. Usually, the upper the chance, the upper the rate of interest the bond pays to compensate buyers for taking over the extra danger.

In contrast to CDs, bonds could be purchased and bought on the secondary market earlier than they mature. This offers liquidity but additionally introduces value danger. If you might want to promote a bond earlier than it matures, its value will rely on the present rate of interest setting and the issuer’s creditworthiness. If rates of interest have risen since you acquire the bond, its worth can have fallen, and also you’ll get lower than what you paid in case you promote.

To summarize, whereas each CDs and bonds are instruments for producing revenue, they operate in another way. CDs are time deposits with banks or credit score unions, providing mounted, insured returns, very best for short-to-medium-term monetary targets. Bonds are basically loans to companies, municipalities, or the federal government. They provide variable returns (normally larger than CDs) and carry completely different ranges of danger, which makes them appropriate for a wider vary of funding methods and timelines.

What’s the Distinction Between CD and Bond? A Detailed Comparability

Security

CDs and bonds are thought-about comparatively secure. CDs, being insured by the FDIC or NCUA, provide a assured return in your principal as much as the insured quantity. Bonds’ security, then again, is dependent upon the issuer’s creditworthiness. Authorities-issued bonds are usually thought-about safer than company bonds.

Minimal Funding Necessities

Bonds usually require larger minimal investments than CDs, generally going into the hundreds of {dollars}. CDs, nevertheless, could be opened with a number of hundred {dollars}, making them extra accessible to buyers with much less capital.

Liquidity

Bonds usually provide extra liquidity than CDs. If you might want to money in your funding, you possibly can promote bonds earlier than their maturity date and not using a penalty. However, you could get lower than the face worth if bond costs have fallen. Contrariwise, CDs impose an early withdrawal penalty, making them much less liquid.

Issuers and Safety

CDs are issued by banks and credit score unions and are insured by the FDIC or NCUA. This insurance coverage protects your funding even when the establishment fails. For bonds, the mechanics are fairly completely different: they’re issued by companies, municipalities, and the federal authorities. The security of your bond funding primarily is dependent upon the creditworthiness of the issuer.

Returns

Bonds usually present larger returns than CDs, relying on the kind of bond and the issuer’s creditworthiness. This potential for larger returns comes with an elevated danger. CDs provide a hard and fast rate of interest and decrease danger however usually yield decrease returns.

Penalties

In the event you withdraw cash from a CD earlier than its maturity date, you’ll incur an early withdrawal penalty. This may eat into your earned curiosity and generally even your principal. Bonds would not have early withdrawal penalties, however in case you promote a bond earlier than its maturity date, its worth could be lower than your authentic funding if bond costs have fallen.

Dangers

Whereas each CDs and bonds are thought-about low-risk investments, they’ve their distinctive dangers. CDs include reinvestment danger, which is the chance that when your CD matures, you will have to reinvest your cash at a decrease rate of interest. Bonds, then again, carry rate of interest danger, which implies that if rates of interest rise, bond costs will fall, and vice versa.

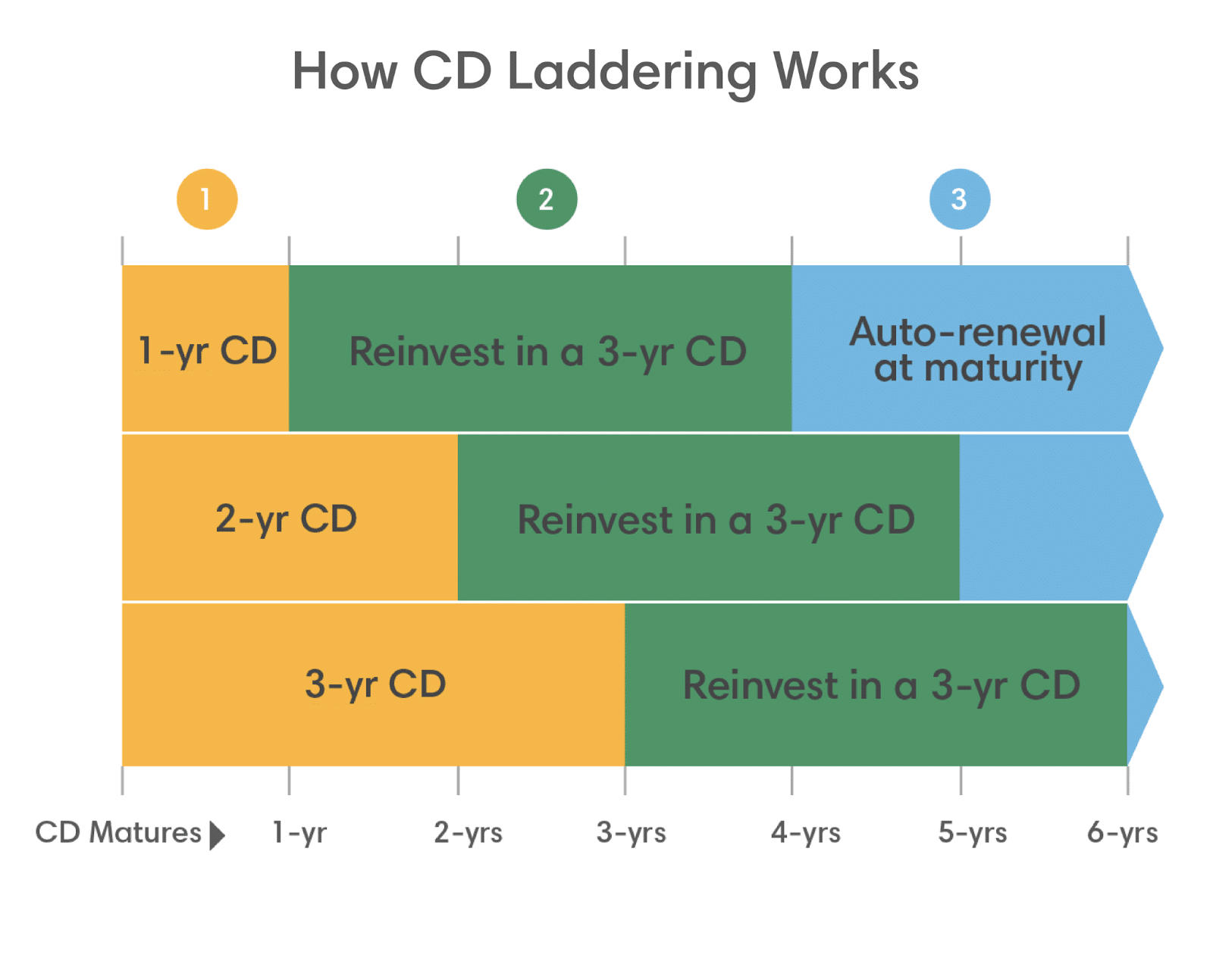

The “Laddering” Method for Investing in Bonds and CDs

Understanding find out how to handle your funding in bonds and CDs could make a major distinction in your return and total expertise. In my experience, some of the efficient methods is the “Laddering” method.

When deciding between CDs vs bonds, the technique of laddering may very well be an efficient technique to stability the liquidity and rate of interest dangers of each these fixed-income investments.

Let’s first make clear what precisely laddering is. Whenever you “ladder” your CDs or bonds, you’re basically diversifying your investments throughout completely different maturity dates. Think about this technique as a ladder the place every rung represents a special maturity date, and the peak corresponds to the size of the funding time period.

For example, as an alternative of investing $15,000 right into a single five-year CD, you may unfold the funding throughout 5 CDs, every maturing one 12 months aside. So, you would possibly buy 5 CDs value $3,000 every with phrases of 1, two, three, 4, and 5 years. That is your ladder.

Now let’s transfer on to why I take into account this a robust technique. Firstly, laddering reduces the impression of rate of interest fluctuations. If your whole cash is tied up in a single long-term CD or bond, and rates of interest rise, you miss out on these larger charges. Nonetheless, with a laddered portfolio, a few of your investments mature earlier, permitting you to benefit from rising rates of interest by reinvesting at these larger charges.

Secondly, laddering can present a degree of liquidity that one usually doesn’t affiliate with CDs and bonds. As every “rung” of your ladder matures, you will have the choice to entry your cash if wanted, with out incurring early withdrawal penalties that may usually be related to accessing a single long-term CD or bond prematurely.

Utilizing my information, I might recommend laddering for individuals who wish to put money into CDs or bonds but additionally wish to mitigate rate of interest danger and preserve some liquidity. This method creates a stability between having fun with the upper charges provided by long-term investments and the pliability of short-term ones.

In conclusion, based mostly on my experience within the subject, I might suggest the laddering method as a balanced, strategic technique of investing in CDs and bonds. This method permits you to seize excessive rates of interest, offers common entry to funds with out penalties, and reduces the chance of locking your complete funding at low charges. Nonetheless, as with all funding methods, it’s important to think about your monetary state of affairs, danger tolerance, and funding targets.

Though each are thought-about safer investments, the important thing distinction in a CD vs a treasury bond dialogue lies in liquidity — CDs usually incur penalties for early withdrawal, whereas treasury bonds could be bought on the secondary market. A CD nonetheless may very well be a more sensible choice than a treasury bond in case you choose to speculate with a financial institution or credit score union and worth the FDIC or NCUA insurance coverage.

Bond vs. CD: FAQs

Are you able to lose cash investing in CDs?

In principle, you can’t lose your principal in a CD as it’s insured by the FDIC or NCUA. Nonetheless, an early withdrawal penalty might scale back your total return and, in some instances, eat into your principal.

That are the very best bonds to purchase now?

The perfect bonds to purchase rely in your funding targets and danger tolerance. Authorities bonds are very secure however provide decrease returns. Company bonds provide larger potential returns however carry extra danger. Diversifying your bond investments, like investing in bond mutual funds, may very well be a great technique to stability danger and reward.

What is best, a CD or a bond?

The selection is dependent upon your monetary targets, danger tolerance, and the timeframe for whenever you would possibly want entry to your funds. In the event you’re on the lookout for a safer, low-risk choice and may afford to depart your funding untouched for a selected interval, a CD could be higher. In the event you want extra flexibility and the potential for larger returns, a bond may very well be a superior alternative.

Are bonds extra liquid than CDs?

Sure, bonds are usually extra liquid than CDs. You’ll be able to promote bonds earlier than their maturity date on the secondary market with out incurring a penalty. Then again, in case you withdraw cash from a CD earlier than its maturity date, you’ll face an early withdrawal penalty. It’s value holding in thoughts, although, that the quantity you get on your bond could be lower than its face worth if bond costs have fallen.

Are bonds or CDs riskier?

Whereas each are thought-about comparatively low-risk investments, bonds could be riskier than CDs. The chance related to bonds largely is dependent upon the creditworthiness of the issuer. For example, company bonds can carry a danger of default. CDs, nevertheless, are insured by the FDIC or NCUA, guaranteeing the return of your principal as much as the insured quantity, making them much less dangerous.

Is a CD an asset?

Sure, a CD is taken into account an asset. Whenever you buy a CD, you might be basically lending cash to a financial institution or a credit score union for a set interval, and in return, you obtain a assured quantity of curiosity. This funding, together with each the unique deposit and the earned curiosity, is a part of your monetary property.

The Backside Line

CDs and bonds provide helpful methods to diversify your funding portfolio. CDs are higher fitted to risk-averse buyers who desire a assured return and don’t want fast entry to their funds. Bonds can provide larger potential returns; they’re fitted to buyers on the lookout for common revenue and the pliability to promote earlier than maturity.

Earlier than investing, keep in mind to concentrate to prevailing and anticipated future rates of interest. If charges are anticipated to rise, short-term bonds or CDs could also be helpful as they might can help you reinvest at larger charges sooner. If charges are predicted to fall, longer-term CDs or bonds could also be extra engaging — they might allow you to lock in a better charge for an extended interval.

Most significantly, perceive your danger tolerance and monetary targets earlier than investing, and take into account in search of recommendation from a monetary advisor in case you’re uncertain. Glad investing!

References

https://www.bankrate.com/banking/cds/how-do-cds-work/ https://investor.vanguard.com/investor-resources-education/understanding-investment-types/what-is-a-bond https://www.dbs.com.sg/private/investments/fixed-income/understanding-bonds# https://www.investor.gov/introduction-investing/investing-basics/investment-products/certificates-deposit-cds https://mint.intuit.com/weblog/investments/money-market-vs-cd/ https://www.idiot.com/investing/how-to-invest/bonds/

Disclaimer: Please notice that the contents of this text aren’t monetary or investing recommendation. The data offered on this article is the writer’s opinion solely and shouldn’t be thought-about as providing buying and selling or investing suggestions. We don’t make any warranties concerning the completeness, reliability and accuracy of this info. The cryptocurrency market suffers from excessive volatility and occasional arbitrary actions. Any investor, dealer, or common crypto customers ought to analysis a number of viewpoints and be conversant in all native laws earlier than committing to an funding.

The submit CDs vs. Bonds: Which Is a Higher Funding? A Complete Information appeared first on Cryptocurrency Information & Buying and selling Ideas – Crypto Weblog by Changelly.

[ad_2]

Source link