[ad_1]

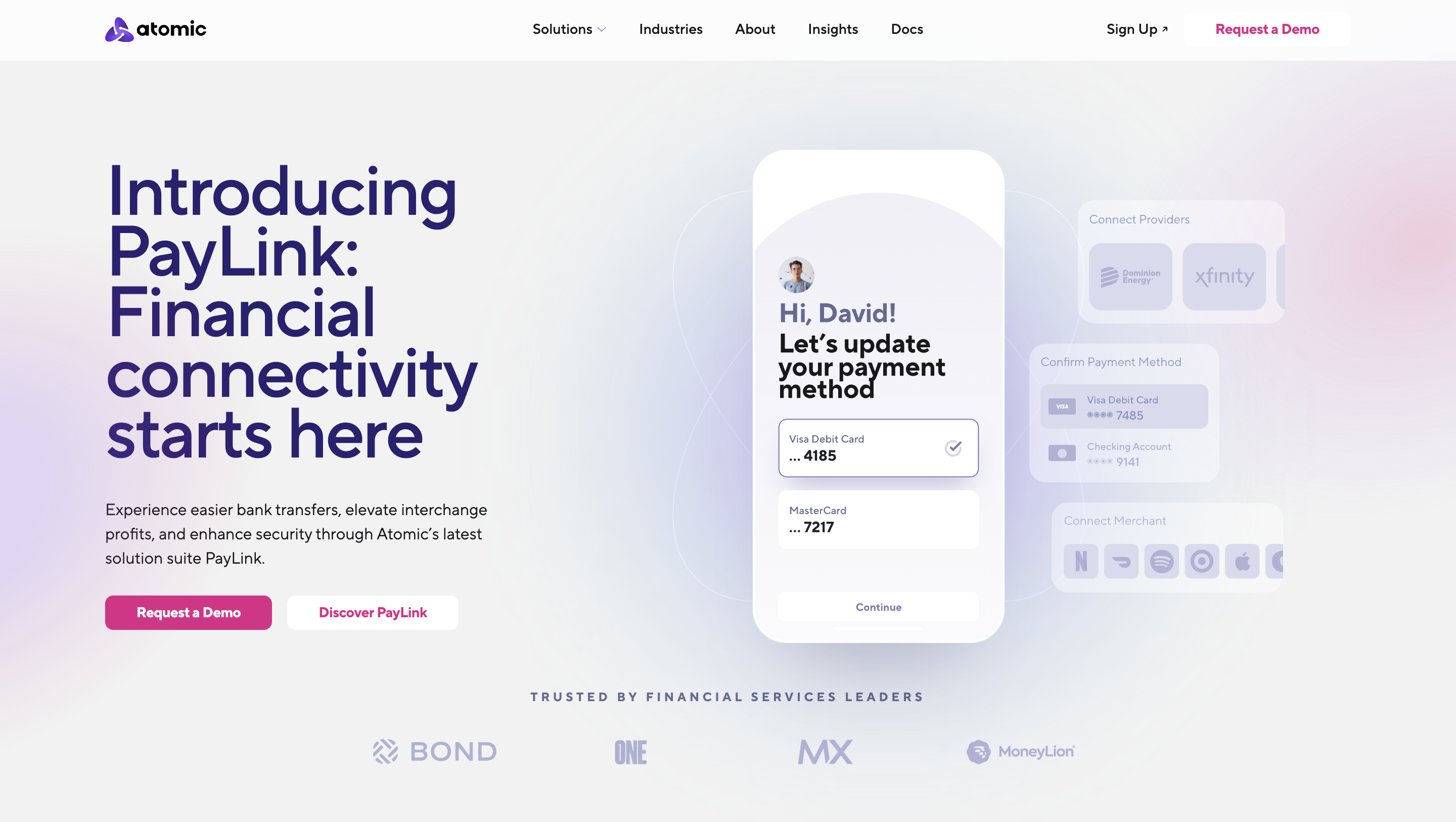

What’s the way forward for open banking within the U.S.? At present, monetary connectivity innovator Atomic launched PayLink, a brand new suite of options that streamline cost switching for customers.

The brand new providing supplies for an improved consumer expertise for monetary companies customers. Additionally it is a giant step in the direction of serving to banks and different monetary establishments align themselves with the Shopper Monetary Safety Bureau’s objectives as regards to open banking.

We talked with Andrea Martone, Head of Product for Atomic, to be taught extra about PayLink, and the drive towards a extra open banking system within the U.S.

Headquartered in Salt Lake Metropolis, Utah, and based in 2019, Atomic made its Finovate debut two years in the past at FinovateFall 2021. Jordan Wright is co-founder and CEO.

Congratulations on the launch of PayLink. Inform us extra about this new suite of merchandise.

Andrea Martone: Thanks! We’re thrilled concerning the launch of PayLink. We’ve taken our experience in constructing user-permissioned connectivity for sharing and updating knowledge and expanded it to service provider accounts, streaming companies, and recurring invoice suppliers, enabling customers to seamlessly replace their cost strategies on file and retrieve data on upcoming funds. Constructing PayLink was a pure subsequent step on our journey in the direction of serving to customers replace their major banking relationship because it helps overcome a significant level of friction within the course of. To construct it, we leveraged our cutting-edge TrueAuth know-how that enables customers to authenticate straight on their units, with out ever sharing login credentials.

For our readers who’re new to Atomic, are you able to inform us slightly concerning the firm?

Martone: At Atomic we imagine that making it easy for customers to entry, share, and replace their monetary knowledge is essential to unlocking new monetary alternatives. By embedding Atomic’s SDK into their on-line and cell banking purposes, monetary establishments can allow customers to simply replace direct deposit directions, confirm revenue and employment, import W2s and, now, replace cost strategies on file with retailers with out leaving their software. With our options, monetary establishments assist develop new account adoption, qualify debtors, and streamline tax submitting.

Open banking was a significant subject of dialog at our FinovateFall convention just a few weeks in the past. What’s your tackle the state of open banking within the U.S.?

Martone: Open banking within the U.S. is at an fascinating juncture. With the CFPB taking daring steps of their public commentary, there’s an thrilling momentum constructing across the consumer-centric transformation of monetary companies. Whereas Europe has been forward on this race, the U.S. is catching up, and I imagine we’re headed for an ecosystem that enables for vital improvements to assist each customers and monetary establishments.

One of many points that got here up in our dialogue on open banking was the concept open banking is integrally associated to the problem of digital identification. Do you agree? Why is that this so and why is it vital to remember?

Martone: Digital identification is the spine of a safe open banking ecosystem. As we democratize entry to monetary knowledge, establishing safe, verifiable digital identities turns into essential. It’s not nearly sharing knowledge, however making certain that the suitable knowledge will get shared with the suitable entities for the suitable functions – securely. Our TrueAuth know-how, for instance, is designed to boost credential safety whereas empowering customers.

The CFPB is engaged on rules that might affect private knowledge rights. What are your ideas on these potential rules and their affect on corporations within the open banking area – in addition to the affect on client adoption of open banking?

Martone: I view the CFPB’s deal with private knowledge rights as a essential step towards fostering a good, clear monetary ecosystem. Giving customers higher portability over their monetary knowledge opens the door for elevated innovation and competitors within the monetary companies area. Nonetheless, it additionally creates a wider floor space for exploitation and misuse of knowledge, as effectively. Consequently, rules might want to set the requirements that guarantee client privateness and knowledge safety and, in flip, construct client belief. For corporations evolving into the open banking area, this is a chance to align their merchandise with consumer-centric values, which I imagine will speed up client adoption and loyalty in the long term.

Atomic is headquartered in Salt Lake Metropolis, Utah. We’ve seen a shocking variety of revolutionary fintechs headquartered in Utah. What’s it prefer to be a tech startup within the Beehive State?

Martone: Being headquartered in Utah has been implausible for us. The state provides a thriving tech scene, a extremely expert workforce, and a business-friendly surroundings. We even have a dynamic workforce positioned all through the nation, which ensures that we comprise a various workforce.

What can we anticipate to see from Atomic over the following few months and into subsequent yr?

Martone: We’ve got a busy roadmap forward! You’ll be able to anticipate to see extra superior options being rolled into PayLink, additional strengthening its capabilities. Additionally, you will see us double-down on our strengths in increasing connectivity the place it will possibly profit customers to entry, share, and replace knowledge in safe, clear, and dependable methods to develop their monetary alternatives. Key to that is persevering with to advance our authentication strategies, together with our TrueAuth know-how. Moreover, we’ll be specializing in strategic partnerships to widen our attain. Our intention is to proceed main the cost in making open banking a tangible, helpful actuality for all.

Photograph by Stephen Leonardi

Associated

[ad_2]

Source link